Building Awning Depreciation

Accelerate Depreciation Deductions With A Cost Segregation Study Blue Co Llc

Accelerated Depreciation Eligibility Gardner Loutzenhiser And Ryan P C

A Cost Segregation Study Can Accelerate Depreciation Deductions

A Cost Segregation Study Can Accelerate Depreciation Deductions Thompson Greenspon Cpa

Https Pgelawsuit Com Wp Content Uploads 2017 12 Personal Property Claim Guide Pdf

Acv Vs Rcv Office Of Public Insurance Counsel Opic

Signage if not related to building operation such as exit signs 8.

Building awning depreciation.

Accelerate Depreciation Deductions With A Cost Segregation Study Weaver Assurance Tax Advisory Firm

Design Guide For Awnings And Canopies Awnex

Curtains Draperies Curtains Awnings Depreciation Calculator Claims Pages

Tax Tactics Spring 2017 Meyers Brothers Kalicka

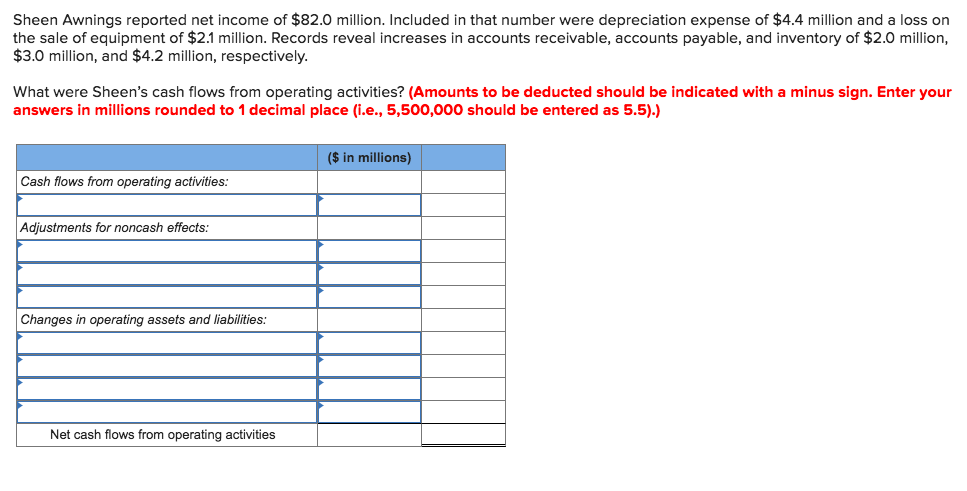

Solved Sheen Awnings Reported Net Income Of 82 0 Million Chegg Com

Add Decors To Your Exterior With 20 Awning Ideas Home Design Lover Modern Exterior Exterior Design House Exterior

With Regards To Replacement Cost Which Insurance Carriers Provide The Full Replacement Cost For A Roof Claim Regardless Of Roof Age And Which Carriers Depreciate The Value Of The Roof Over Time

Cares Act Expands Bonus Depreciation To Qualified Improvement Property Elliott Davis

Reasons For The Awning Getting Torn And Rv Awning Repair In This Case Rv Travel Trailer Rvs Campers Tenttrai Camper Awnings Rv Awning Fabric Rv Lighting

Image Result For How To Build An Awning Over A Door Door Awnings Diy Awning Front Door Canopy

Simple Black Fabric Awning Classic Storefront Design Front Building Design Facade Design

Building An Awning Diy Awning Porch Awning Porch Roof

Diy Free Plans For Building Wooden Window Awnings Wooden Pdf Photos Of Pergolas Window Awnings Windows Exterior Timber Windows

Roof Replacement Depreciation Roofrepair Copper Gutters Gutters Roofing

Accelerate Depreciation Deductions With A Cost Segregation Study Suttle Stalnaker Cpas

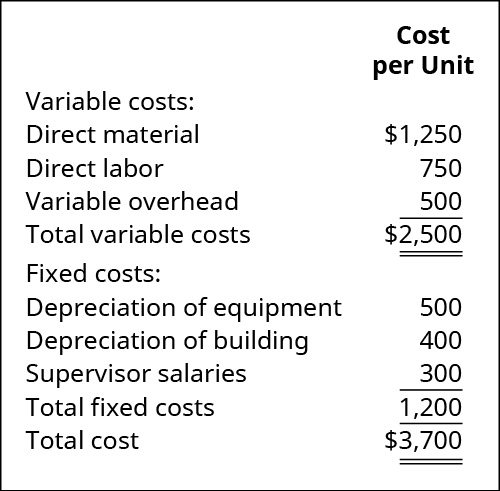

Evaluate And Determine Whether To Make Or Buy A Component Principles Of Accounting Volume 2 Managerial Accounting

Custom Metal Building With Awning Jpg 650 373 Metal Buildings Custom Metal Buildings Metal Building Kits

How To Build An Awning Over A Door Google Search Timber Frame Porch House Exterior Porch Timber

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcsd4elarsf3mkybeacao1oles1 Btbcchlwv5v9ph7z7 Car4 E Usqp Cau

Rock Work And Porches Mobile Home Porch Mobile Home Exteriors Manufactured Home Porch

Awnings Dallas Fort Worth Commercial Metal Building Exterior House Exterior Exterior Design

How Much Does A Mobile Home Depreciate Each Year

Home Business Vacation Certificates 726 20180912134219 49 Small Home Business In Qatar Doha Malls Work From Home Business Home Business Manufactured Home

Panoramio Photo Of Lindey S Columbus Restaurants Ohio Travel German Village

Source : pinterest.com